Thomson Reuters Reminds Non-Canadian Taxable Shareholders of "Opt-Out" Alternative for Return of Capital

PR Newswire

TORONTO, April 14, 2026

Action is required to opt out

Opt-out deadlines vary by intermediary and may be earlier than April 27, 2026

TORONTO, April 14, 2026 /PRNewswire/ -- Thomson Reuters (TSX/Nasdaq: TRI) today reminded its shareholders who are taxable in a jurisdiction outside of Canada that they can "opt out" of the company's proposed return of capital. For shareholders who are subject to income tax outside Canada, opting out of the return of capital may be preferable to participating in the return of capital.

As described in the company's management proxy circular dated March 13, 2026 (the "Circular"), the proposed return of capital and share consolidation transactions consist of a special cash distribution of US$605 million in the aggregate, or approximately US$1.36 per common share (estimated based on the number of common shares issued and outstanding as of March 6, 2026 and assuming no shareholders opt-out of the return of capital), and a consolidation of the company's outstanding common shares (or "reverse stock split") on a basis that is proportional to the special cash distribution.

The return of capital is intended to distribute cash on a basis that is generally expected to be tax-free for Canadian tax purposes. As a result, Canadian resident shareholders are generally not eligible to opt out of the return of capital. Eligibility criteria for opting out of the return of capital is set out below.

Opting out

- What happens if you opt out: If you're eligible to opt out of the return of capital and choose to do so, you will not receive the special cash distribution. Each opting-out shareholder will still participate in the proposed transactions through a share exchange and the share consolidation but will continue to hold the same number of shares that it currently holds. Such opting-out shareholders will realize a proportionate increase in their equity and voting interests in the company by virtue of the consolidation of the participating shares under the share consolidation.

- Process: If you're a non-registered holder (i.e., you hold shares through a bank or broker), follow your bank or broker's instructions if you'd like to opt out of the return of capital. You should contact your bank or broker if you have not received information regarding how to opt out of the return of capital. Registered shareholders should follow instructions sent to them by Computershare Trust Company of Canada, including depositing with Computershare a duly completed opt-out election and certification form prior to 5:00 p.m. EDT on April 27, 2026.

- Deadline: Any opt-out elections should be completed by the deadline set by your bank/broker or Computershare (depending on whether you're a non-registered or registered holder).

If you're not eligible to opt out of the return of capital or are eligible to opt out but decide not to, no action is required to participate in the return of capital.

Tax Consequences

The Canadian and U.S. tax consequences of the proposed return of capital and share consolidation transactions are complex. Shareholders are encouraged to review the Circular and related materials carefully and to consult their financial, tax and legal advisors before making a decision with respect to the transactions, including any decision to opt out of the return of capital.

Conversion and Share Consolidation Ratios

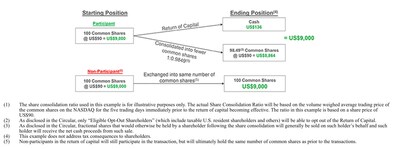

Pursuant to the terms of the plan of arrangement to implement the return of capital and share consolidation transactions, each issued and outstanding non-participating share will be exchanged for one New Common Share and, after the return of capital to participating shareholders, each issued and outstanding New Common Share will be exchanged for a number of common shares equal to the Conversion Ratio and each issued and outstanding common share will then be consolidated into a number of post-consolidation shares equal to the Share Consolidation Ratio. Accordingly, non-participants in the return of capital will still participate in the share consolidation but will ultimately hold the same number of common shares as prior to the transactions, and participating shareholders will hold a fewer number of common shares to reflect the return of capital received.

Below is a description of the Conversion and Share Consolidation Ratios, as well as a numerical example:

The "Conversion Ratio" will be calculated as follows:

|

1 |

where X is the volume weighted average trading price of Thomson Reuters shares on the Nasdaq for the five trading days on which Thomson Reuters shares trade on the Nasdaq immediately preceding the effective date of the transactions. |

The "Share Consolidation Ratio" will be calculated as follows:

|

$X-Cash Distribution Per Share |

where X is the volume weighted average trading price of Thomson Reuters shares on the Nasdaq for the five trading days on which Thomson Reuters shares trade on the Nasdaq immediately preceding the effective date of the transactions. |

The Conversion and Share Consolidation Ratios will be fixed after close of business on the last trading day preceding the effective date of the transactions in order to allow Thomson Reuters to consolidate the common shares on a basis that is proportional to the return of capital distribution.

The foregoing discussion of the Conversion and Share Consolidation Ratios is intended to provide a general summary only. Shareholders are encouraged to read the Circular in its entirety.

Additional information and assistance

To be eligible to opt out of the return of capital, a shareholder must be an "Eligible Opt-Out Shareholder," which means a shareholder (whether registered or non-registered) who is (a) not a resident of Canada for Canadian federal income tax purposes and is subject to income tax in a jurisdiction other than Canada (and is not exempt from income tax in that jurisdiction) or (b) an individual who is a resident of Canada for Canadian federal income tax purposes and who is also subject to income tax in a jurisdiction other than Canada as a resident of that other jurisdiction (and is not exempt from income tax in that other jurisdiction).

Details of the return of capital and share consolidation transactions (including information regarding the opt-out right and tax considerations) are described in the Circular and related materials, which are available on www.thomsonreuters.com in the "Investor Relations" section. The documents were filed with the Canadian securities regulatory authorities on SEDAR+ and are available at www.sedarplus.com. The documents were also furnished to the U.S. Securities and Exchange Commission through EDGAR and are available at www.sec.gov.

Registered shareholders who have questions or need assistance may contact Computershare Investor Services Inc. at 1.800.564.6253 (toll-free in Canada and the U.S.) or at 1.514.982.7555 (outside Canada and the U.S.).

Non-registered shareholders who hold their shares indirectly through an intermediary (such as an investment dealer, stock broker, bank, trust company or other nominee) should contact their intermediary if they have questions or need assistance.

Shareholders who have questions or need assistance may also contact D.F. King & Co., Inc., who is acting as Information Agent for the transactions at 1.800.967.5068 (toll-free in Canada and the U.S.) or at 1.212.561.5870 (outside Canada and the U.S., banks, brokers and collect calls) or at the following email address: tri@dfking.com.

About Thomson Reuters

Thomson Reuters (TSX/Nasdaq: TRI) informs the way forward by bringing together the trusted content and technology that people and organizations need to make the right decisions. The company serves professionals across legal, tax, audit, accounting, compliance, government, and media. Its products combine highly specialized software and insights to empower professionals with the data, intelligence, and solutions needed to make informed decisions, and to help institutions in their pursuit of justice, truth and transparency. Reuters, part of Thomson Reuters, is the world's leading provider of trusted journalism and news. For more information, visit thomsonreuters.com.

SPECIAL NOTE REGARDING FORWARD-LOOKING STATEMENTS

Certain statements in this news release are forward-looking within the meaning of applicable Canadian and U.S. securities laws, including the Private Securities Litigation Reform Act of 1995, including statements relating to the return of capital and share consolidation transactions and the anticipated tax treatment for shareholders participating in the return of capital and those opting out. These forward-looking statements are based on certain assumptions, including shareholder approval of the transactions, and reflect our company's current expectations. As a result, forward-looking statements are subject to a number of risks and uncertainties that could cause actual results or events to differ materially from current expectations, including the risk factors discussed in materials that Thomson Reuters from time to time files with, or furnishes to, the Canadian securities regulatory authorities and the U.S. Securities and Exchange Commission. There is no assurance that the return of capital and share consolidation transactions will be completed or that other events described in any forward-looking statement will materialize. Except as may be required by applicable law, Thomson Reuters disclaims any obligation to update or revise any forward-looking statements.

CONTACTS

MEDIA

Zoe Zanettos

Director, Corporate Affairs

+1 647 202 8948

zoe.zanettos@thomsonreuters.com

INVESTORS

Gary E. Bisbee, CFA

Head of Investor Relations

+1 646 540 3249

gary.bisbee@thomsonreuters.com

![]()

![]() View original content to download multimedia:https://www.prnewswire.com/news-releases/thomson-reuters-reminds-non-canadian-taxable-shareholders-of-opt-out-alternative-for-return-of-capital-302742301.html

View original content to download multimedia:https://www.prnewswire.com/news-releases/thomson-reuters-reminds-non-canadian-taxable-shareholders-of-opt-out-alternative-for-return-of-capital-302742301.html

SOURCE Thomson Reuters